Neural Financial Market Factors

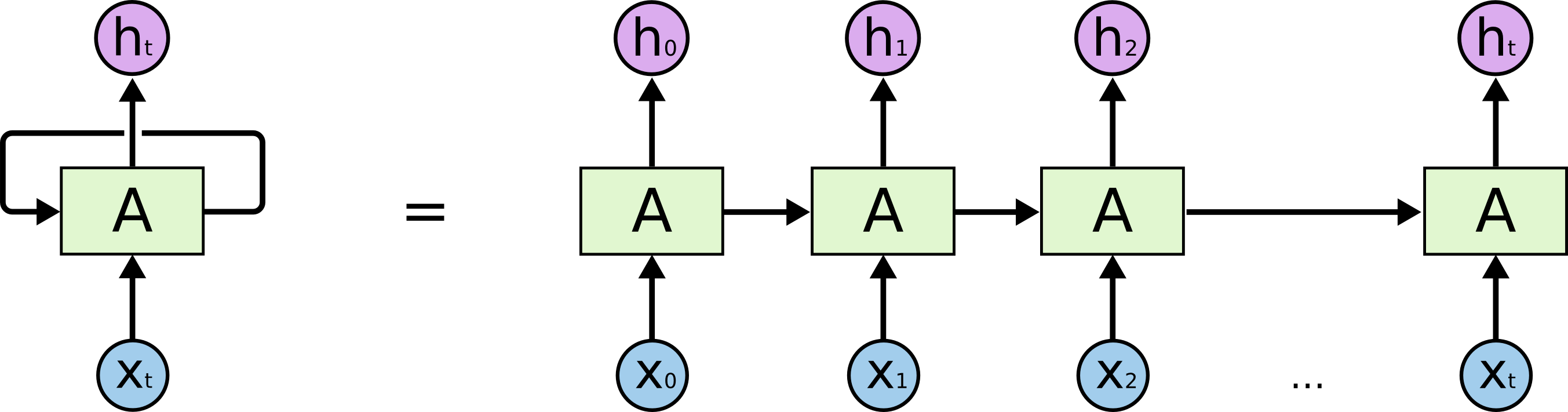

We could give (multi-) series of data to LSTM, at every step feeding the observations obtained for that step. An illustration of the architecture of LSTM is given below. (Courtesy: https://colah.github.io)

$h_t$ is the Hidden or System state at every moment $t$. The key idea is to minimise a certain distance metric

\[\phi(Wh_t,W_{\text{port}}x_{t+1})\]with certain regularisation.